To know what is NPS and basic introductory details on the same, go to the previous post using the link given here.

Okay. I will be getting more than (at least risk-free?) 8% always right?

Simply, What are the benefits and returns in NPS?

Short Answer. No. There are many Pension Fund Management companies which will be managing your money on your behalf to get you returns for your Pension. It is again your choice to select the Pension Fund Management Companies. Based on the choice of the fund (Auto-Choice/Active Choice),

the returns has historically varied from 4% -26%.

But this cannot guarantee this will always give positive returns, as it have some equity exposure (for Active Choice, Asset Class E). But in the long run certainly, equities tend to outperform the debt and is always better.

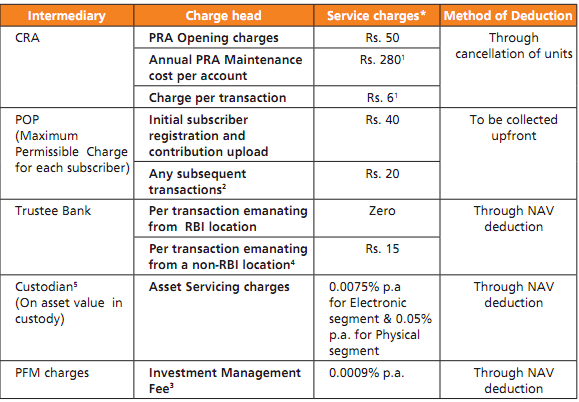

Charges:

Remember this rule: If you invest more in NPS, you will end up having less charges as the charges are more or less static per year and the Fund Management charge is very less.

Okay. I will be getting more than (at least risk-free?) 8% always right?

Simply, What are the benefits and returns in NPS?

Short Answer. No. There are many Pension Fund Management companies which will be managing your money on your behalf to get you returns for your Pension. It is again your choice to select the Pension Fund Management Companies. Based on the choice of the fund (Auto-Choice/Active Choice),

the returns has historically varied from 4% -26%.

But this cannot guarantee this will always give positive returns, as it have some equity exposure (for Active Choice, Asset Class E). But in the long run certainly, equities tend to outperform the debt and is always better.

Charges:

Remember this rule: If you invest more in NPS, you will end up having less charges as the charges are more or less static per year and the Fund Management charge is very less.

|

| Charges - NPS |

Compare the Fund Management charge with the index fund's Fund Management charge of 1.35%.

The Maintenance cost is similar to the demat account maintenance cost. In addition to above, demat charges will be applicable.

You can choose to have the 80% of the complete amount as the annuity and 20% in the fund as the lump-sum amount at the end of 60 or 70 as per your choice. The last year can be extended after due consideration and it is 70 years as of writing this article.

If you are not able to pay the minimum in any of the year, you have to pay an additional Rs.100/- as penalty to renew the account and the account becomes dormant otherwise.

The above details are completely for the Tier-I NPS account. This is the primary pension account introduced by NPS. This is of course illiquid.

If one has Active Tier-I NPS account and want to use the NPS account for the short term as well, he can use the Tier-II NPS account.

For opening Tier-II NPS account, there should be Tier-I active NPS account.

Minimum while opening: Rs. 1000/-

Minimum per instance: Rs. 250/-

Minimum Account Balance at the end of FY: Rs. 2000/-

At-least one contributions in a year.

This Tier-II is a voluntary savings attached with Tier-I and not mandatory.

Comments

Post a Comment